In addition to research and teaching, I collaborate with international organisations as well as with the media. Several recent examples follow.

To date, I have accepted invitations to speak at the European Parliament’s public hearings four times: 2019, 2020, 2022, and 2025.

On May 15, 2025, I gave a presentation “The End of Tax Avoidance by Multinationals?” and participated actively in a discussion at the FISC public hearing “The 2 Pillar framework in view of international developments and the EU-US relations“.

On October 27, 2022, I contributed to the FISC public hearing on “The Reform of Corporate Taxation: What’s Next?” – the video and other documents are available here.

On December 1, 2020, I contributed to the FISC public hearing on “Do harmful tax practices within and outside the EU create distortions of competition in the Single Market?” – the video and other documents are available here.

I also accepted the invitation to take part in the European Parliament’s TAX3 committee public hearing on “The evaluation of the Tax Gap” on January 24, 2019. The video and other documents are available here.

In May 2024, the final communiqué of the G7 Finance Ministers and Central Bank Governors’ meeting was presented by Italy. One of its annexes, 2024 Progress Report on Tax Co-operation for the 21st Century: OECD Report for the G7 Finance Ministers and Central Bank Governors, cited one of my research papers.

In a January 2024 United States Senate Budget Committee hearing on “The Great Tax Escape: Closing Corporate Loopholes that Reward Offshoring Jobs and Profits”, several academic witnesses cited my research paper Did the Tax Cuts and Jobs Act Reduce Profit Shifting by US Multinational Companies? with Javier Garcia-Bernardo and Gabriel Zucman and Kimberly Clausing also cited my research paper Fiscal Consequences of Corporate Tax Avoidance with Katarzyna Bilicka and Evgeniya Dubinina.

The Economist used a graph from my research paper in 2022:

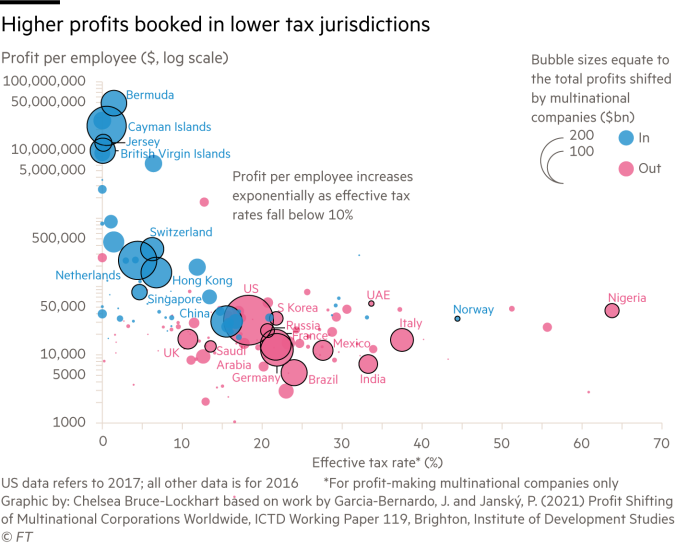

The Financial Times used a graph from my research paper in 2021:

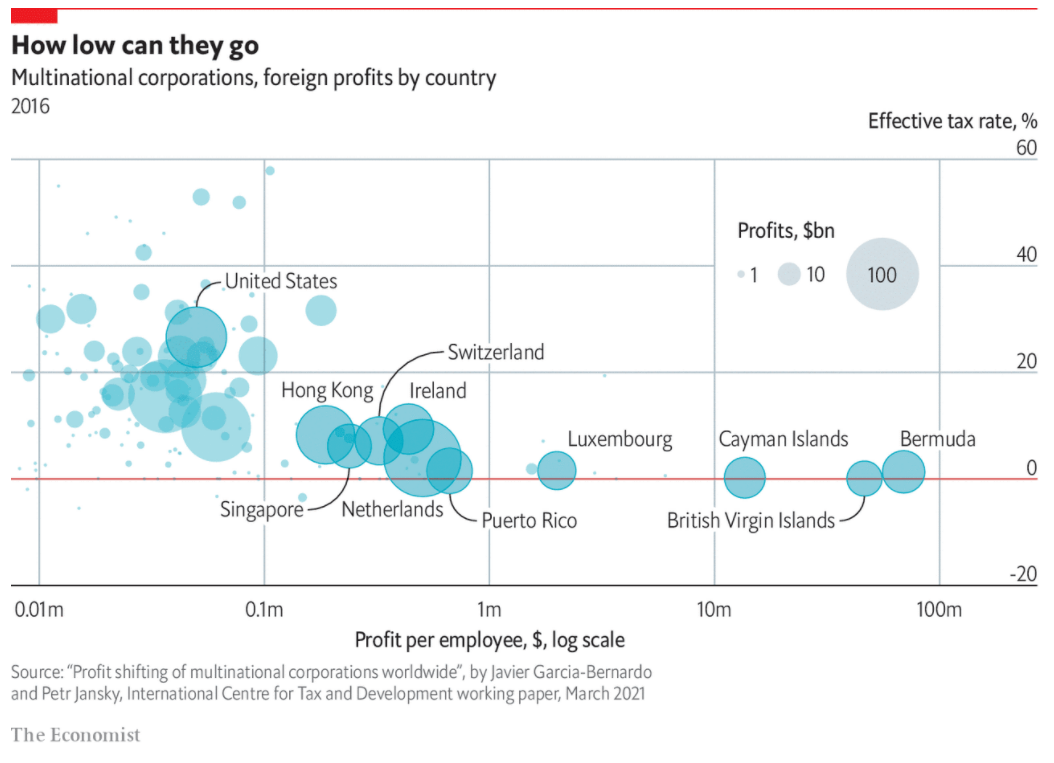

The Economist used a graph from my research paper in 2021:

My research has been repeatedly cited by leading newspapers including The Economist also in earlier years:

The Economist in January 2019: “Alex Cobham of the Tax Justice Network and Petr Jansky of Charles University, Prague, propose two indicators: one based on mismatches between where multinationals report their profits and where their real activity occurs, and another that is a measure of undeclared offshore assets.”

The Economist in February 2019: “An analysis of American multinationals and their international subsidiaries in 2017 found that the share of profits declared elsewhere for tax purposes had risen from 5-10% in the 1990s to 25%. Poor countries are hit hardest because they rely more on corporate tax revenues than rich countries, and because international tax rules, originally crafted to suit advanced economies, are stacked against them.”

The Economist in November 2011: “A recent independent study by three doctoral students from Charles University—Jana Chvalkovská, Petr Janský and Jiří Skuhrovec—is alarming. Their “zIndex” of public procurement shows that 67% of the €13.7billion ($19 billion) spent between 2006 and 2010 is not tracked in the government’s official procurement database. About 14 % of all tenders during that period (worth some €2 billion) only had one bidder, and none meet the criteria of the OECD and the Regional Development Ministry.”

My research has influenced an indicator of the Sustainable Development Goals on illicit financial flows. Two UN agencies—UNODC and UNCTAD—published a report in October 2020 on Conceptual Framework for the Statistical Measurement of Illicit Financial Flows. The report agrees with a background paper for UNCTAD that I co-authored with Alex Cobham whereby aggressive tax avoidance is included as an illicit financial flow, while noting that such activities are generally legal. Moreover, in a 2020 Oxford University Press book, we proposed an indicator that would rely on OECD country by country reporting to track the scale of corporate tax abuse and the new report highlights exactly that possibility. In addition, the UN High-Level Panel on International Financial Accountability, Transparency and Integrity (UN FACTI Panel) for achieving the 2030 agenda published its interim report in September 2020, which cites some of my research, including the book.![]()